Trusts – are they still worth it?

The recent ATO crackdown on trusts will no doubt have some business owners (and even some advisors) asking themselves the question: Is this structure for business purposes still worth it?

To recap, trust distributions have been under the ATO microscope in recent years. The latest ATO crackdown was in February 2022 when it updated its guidance around trust distributions especially those made to adult children, corporate beneficiaries and entities that are carrying losses.

Depending on the structure of these arrangements, the ATO may potentially take an unfavourable view on what were previously understood to be legitimate distribution arrangements. The ATO is chiefly targeting arrangements under section 100A of the Tax Act; specifically, where trust distributions are made to a low-rate tax beneficiary, but the real benefit of the distribution is transferred or paid to another beneficiary usually with a higher tax rate. In this regard, the ATO’s Taxpayer Alert (TA 2022/1) illustrates how section 100A can apply to the quite common scenario where a parent benefits from a trust distribution to their adult children.

Despite this new ATO interpretation and the wider crackdown on trusts in recent years, the choice of a trust as a business structure still has a range of benefits including:

- Asset protection – limited liability is possible if a corporate trustee is appointed. Usually, when a person owes money and cannot meet the repayment requirements, the creditor can access the person’s personal assets to recoup the debt payable. However, if a trust is in place, there is no access to beneficiary assets.

- 50% CGT discount – A family trust receives a 50% discount on capital gains tax for profits made from selling any assets the trust has held for more than 12 months. This contrasts with a company structure. Companies cannot access the 50% CGT discount.

- Tax planning – Income that sits in the family trust that is not distributed by year-end is taxed at the highest income tax rate. However, any trust income distributed to the beneficiaries is taxed at the income tax rate of the beneficiary who receives the distribution. The way to definitely get around the ATO’s aforementioned section 100A crackdown is to ensure the distributed money actually goes to the nominated beneficiary and is enjoyed by the beneficiary rather than another taxpayer.

- Carry-forward losses – A trust does not distribute losses to beneficiaries. This means the beneficiaries will not be called upon to contribute money to the trust to meet any loss. Instead, losses from each year can be carried forward to the following year, subject to certain conditions being met.

If you have questions around your trust structure, or your business structure more generally, touch base with us.

Time for a restructure?

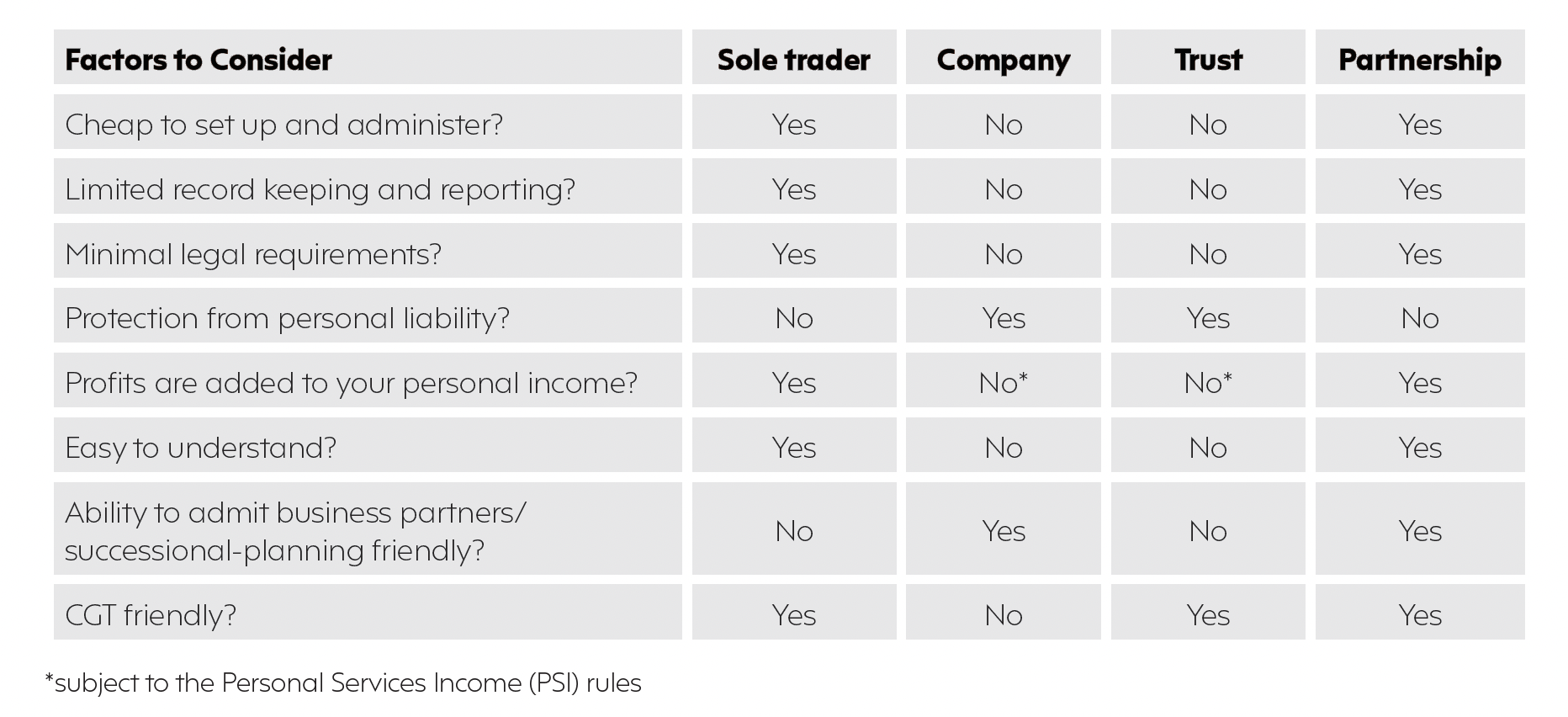

The new financial year can be a time where business owners look at their operating structure and consider whether it still meets their needs. Choosing a structure is not simply about minimising tax, rather a range of factors should be considered as such as asset protection, establishment and ongoing compliance costs, succession planning, and your understanding of each structure etc.

Most small businesses operate as a sole trader, company, trust, or partnership. The following table is a comparative snapshot of each of the four structures:

You may find that, as your business grows or as your priorities change, your chosen structure no longer serves your needs. For example, a number of people commence businesses as sole traders (often for reasons of simplicity as well as keeping start-up costs to a minimum) but later find that this structure is no longer appropriate. From an income tax perspective, a drawback with sole traders is that income from the business is assessed personally to you at your marginal tax rates. As your business grows and the revenue generated increases, your tax rate also increases.

The take-home message is that you should periodically review your structure to ensure it continues to serve your needs. Be mindful however that changing structures can have CGT and stamp duty consequences – these one-off costs need to be taken into account when making the decision whether to change. Also note that under the small business rollover provisions, it may be possible for you to change your structure without incurring CGT.

Talk to us if you are contemplating changing your business operating structure.

Super contribution caps to increase 1st July 2024

For the first time in three years, the superannuation contributions are set to increase from 1 July 2024.

Contribution caps to increase

Due to indexation, the contribution caps will increase on 1 July 2024 as follows:

- Concessional contributions cap – from $27,000 to $30,000

- Non-concessional contributions cap – from $110,000 to $120,000

- The maximum non-concessional contributions cap under the bring forward rules – from $330,000 to $360,000

What are concessional contributions?

Concessional contributions (CC) are before-tax contributions and are generally taxed at 15%. This is the most common type of contribution individuals receive as it includes superannuation guarantee (SG) payments your employer makes into your fund on your behalf. Other types of CCs include salary sacrifice contributions and tax-deductible personal contributions.

The government sets limits on how much money you can add to your superannuation each year. Currently, the annual CC cap is $27,500 in 2023/24.

What are non-concessional contributions?

Non-concessional contributions (NCC) are voluntary contributions you can make from your after-tax dollars. For example, you may wish to make extra contributions using funds from your bank account or other savings.

As such, NCCs are an after-tax contribution because your employer has already taken out the tax you need to pay on your income. Currently, the annual NCC cap is $110,000 in 2023/24.

What are the bring forward rules?

The bring forward rules apply to NCCs and allow you to make up to three years of NCCs in a single financial year, if you’re eligible. This means you can put in up to three times the annual cap of $110,000, which means you may be able to top up your superannuation by $330,000 within the same financial year.

Using the bring forward rules can be beneficial for individuals who have a large amount of cash to invest which may have come from an inheritance or from the sale of an asset/property.

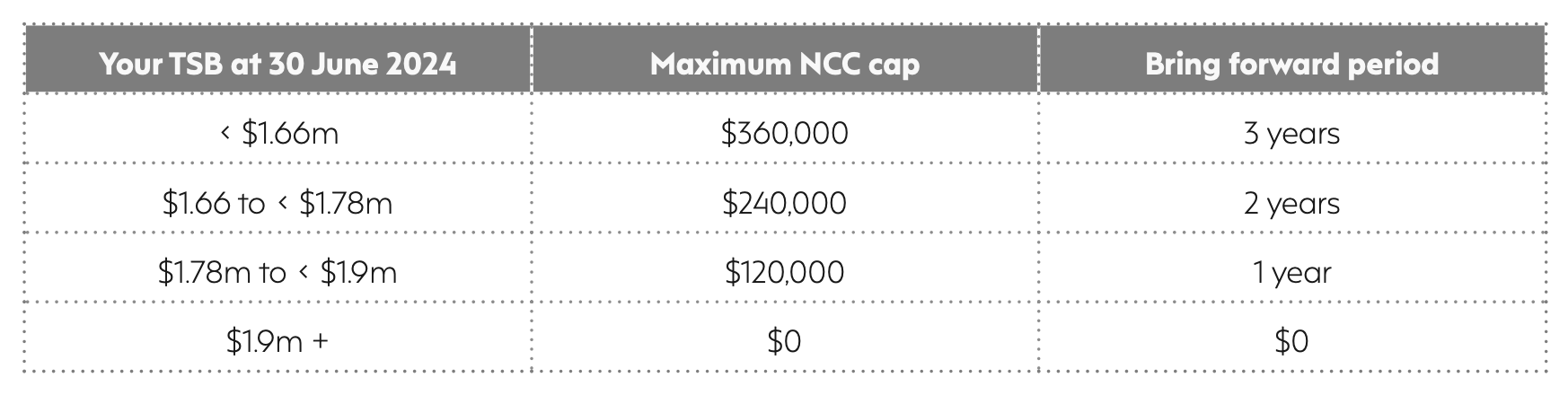

However, how much you can make as a NCC will depend on your total superannuation balance (TSB) as at 30 June of the previous financial year (see table below).

The table below shows the TSB thresholds that apply to determine how much you can contribute under the bring forward rules:

Bring forward NCC amounts will also increase

In addition to the contribution caps increasing, the maximum NCC cap under the bring forward rules will also increase on 1 July 2024.

Take care before you contribute

The increase to the NCC cap under the bring forward rules will not apply to individuals who have already triggered the bring forward rule in either this year (2023/24) or last year (2022/23) and are still in their bring forward period. This is because the NCC cap that applies to an individual is calculated with reference to the standard NCC cap when they triggered the bring forward rule in their first year.

For example, if the NCC cap in the second and third year of a bring forward period changed to $120,000 due to indexation, your NCC cap will still be $330,000 ($110,000 x 3 years) and not $350,000 ($110,000 + $120,000 + $120,000).

For this reason, if you want to maximise your NCCs using the bring forward rule, you may wish to consider restricting your NCCs this year to $110,000 or less so you do not trigger the bring forward rule this year.

However, how much you can contribute and whether your fund is allowed to accept your contribution can depend on your age, your TSB and other eligibility criteria. The rules are complex and making contributions to superannuation that exceed the contribution caps can result in excess tax. Give us a call if you need any further information or would like to chat about your options.

GST refresher for your business

Most businesses are familiar with how GST works. But here’s a few reminders to make sure you’re being compliant and maximising your GST claims.

GST is paid at each step in the supply chain and business charge GST in the price of goods, services or anything else they supply. If an entity is registered for GST, it can claim input tax credits from the ATO for any GST included in the price paid for goods, services or anything else bought for the business. However, for GST registered enterprises, the liability to pay GST rests on the supplier of goods and services, not on the consumer. In other words, even if the business does not include the GST in the price of goods and services supplied, it is still liable to pay it to the ATO.

Coffee or cars anyone?

As we move into a new financial year, you may be thinking of rewarding the office with an impressive new coffee machine for the staff room, or perhaps you are thinking a bit bigger, say a new vehicle. Either way you may want to keep some of these GST issues in mind:

1. Second-hand goods*

Buying second-hand can often be cheaper. However, if you purchase from a non-registered seller (eg, a friend, or privately via Gumtree, eBay etc) unless the seller is a re-seller of second-hand goods registered for GST, in most cases you will not be able to claim GST on the purchase. (And if you are registered for GST, don’t forget to charge GST when you sell your business assets regardless of whether the purchaser is registered for GST or not).

(*excludes goods containing valuable metals)

2. Deposits

The purchase of a significant asset often requires a deposit to be paid. If you report GST on a cash basis, you will not be entitled to claim a GST input tax credit on the deposit at the time of paying (you may be entitled to claim it if you have paid an amount in addition to the deposit, or if you report GST using the non-cash accounting method and hold a tax invoice). If you haven’t claimed GST at the time of paying the deposit, make sure to claim GST on the full purchase price, including the deposit, when the deposit is later applied towards the cost of the asset (which may occur in a later BAS reporting period).

3. Purchasing a car for more than the car limit

Your GST input tax credit will be limited if you purchase a car with a cost that exceeds the tax car cost limit for depreciation. The car cost depreciation limit is the maximum you can claim as depreciation deductions for income tax purposes ($68,108 in 2023-24). Where the cost of your car exceeds this value, your GST claim is limited to 1/11th of the car limit ie, $6,191 (1/11th x $68,108). Importantly, there are some exceptions to this rule where your GST entitlement will not be limited, including on the purchase of a commercial vehicle (those not designed to carry passengers) or motor homes and campervans.

Be aware, however, that on the disposal of the car there is no corresponding reduction or adjustment to the GST on the sale proceeds ie, you must pay the ATO 1/11th of the full sale proceeds. This is the case, even if your GST and depreciation claims were limited on the purchase under these rules.

4. Cancelling your GST registration

A cost that is often overlooked when considering winding up a business is the potential need to repay GST previously claimed in respect of assets you still hold. In most cases (there are a few exceptions), you must cancel your GST registration within 21 days of selling or closing your business. You can also choose to cancel your GST registration if your GST turnover is below the turnover threshold ($75,000). If, when you cancel your GST registration, you still hold business assets on which you previously claimed GST, you may need to repay some of those credits, depending on how long you have owned the asset and its original cost. The adjustment will generally be 1/11th of the GST inclusive value of the asset at the time of cancelling your registration (where this value is lower than its original cost).

Small but not insignificant

It’s not just on these larger transactions where we can uncover GST issues. Although the dollars involved are usually more significant when buying and selling business assets, it is extremely easy to over or under claim GST on our day-to-day transactions and over time, these too can add up to a sizeable GST adjustment. For example:

- Bank fees – ordinary monthly bank account charges won’t include GST, but merchant fees do so check your accounting system is set up to capture the GST on those merchant fees.

- Insurance policies – insurance policies often include a small stamp duty component which does not attract GST. If your accounting software is set up to claim a full 10% GST (or 1/11th of the premium cost) you may be overclaiming GST.

- Recharge or top-up cards – eg, for tolls, telephone (and vouchers given as Christmas or toher gifts) – GST should only be accounted for when the recharge is used or redeemed for purchases used in your business, not when the cards or vouchers are purchased.

- Private apportionment – eligible small businesses can make an annual apportionment of GST where purchases are partly for business and partly for private purposes rather than each time you pay an expense. You can make this adjustment in the activity statement that covers the period your income tax return is due, making sure not to reduce your GST claim twice (once when you paid the expense, and once as part of the annual adjustment).

- Software subscriptions – you may not be claiming GST on software subscriptions on the basis that the supplier is an overseas supplier. However, from 1 July 2017 the rules changed in this area so you may be paying GST when you do not have to, or not claiming GST when you could be – you will need to check your tax invoices and let your bookkeeper or accountant know if the software subscriptions you are paying include GST (or provide the software supplier your ABN so you are not charged in the first instance).

Remember the best way to maximise your GST claims is by checking your tax invoices for GST paid (you have four years to claim the GST), and then keeping those and other GST records for 5 years.

If you have any questions around GST, reach out to us.

The importance of cash flow forecasts

With many economists predicting a slowing of the economy, planning your business’s cashflow is more important than ever.

Studies suggest that the failure to plan cash flow is one of the leading causes of small business failure. To this end, a cash flow forecast is a crucial cash management tool for operating your business effectively.

Specifically, a cash flow forecast tracks the sources and amounts of cash coming into and out of your business over a given period. It enables you to foresee peaks and troughs of cash amounts held by your business, and therefore whether you have sufficient cash on hand to fund your debts at a particular time.

Moreover, it alerts you to when you may need to take action – by discounting stock or getting an overdraft, for example – to ensure your business has sufficient cash to meets its needs. On the other hand, it also allows you to see when you have large cash surpluses, which may indicate that you have borrowed too much, or you have money that ought to be invested.

In practical terms, a cash flow forecast can also:

- make your business less vulnerable to external events in the economy, such as interest rate rises

- reduce your reliance on external funding

- improve your credit rating

- assist in the planning and re-allocation of resources, and

- help you to recognise the factors that have a major impact on your profitability.

At this point, a distinction should be drawn between budgets and cash flow forecasts. While budgets are designed to predict how viable a business will be over a given period, unlike cash flow forecasts, they include non-cash items, such as depreciation and outstanding creditors. By contrast, cash flow forecast focus on the cash position of a business at a given period. Non-cash items do not feature. In short, while budgets will give you the profit position, cash flow forecasts will give you the cash position.

Cash flow forecasting can be used by, and be of great assistance to, the following entities:

- business owners

- start-up business

- financiers

- creditors.

A cash flow forecast is usually prepared for either the coming quarter or the coming year. Whether you choose to divide the forecast up into weekly or monthly segments will generally depend on when most of your fixed costs arise (such as salaries, for example). When you are making forecasts, it is important to use realistic estimates. This will usually involve looking at last year’s results and combining them with economic growth, and other factors unique to your line of business. When forecasting overheads, usually a forecast will list:

- receipts

- payments

- excess receipts over payments (with negative figures displayed in brackets)

- opening balance

- closing bank balance.

Reach out to us if you would like to know more.